The Refinance Treadmill: Lower Payment, Longer Sentence

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

January used to be Rajiv’s tax-saving season: the office declaration deadline, the agent’s call, the hurried ELSS or the insurance premium “for 80C”. This January the ritual repeated — the agent called, the pitch ran, the form was signed. One problem: Rajiv switched to the new tax regime two years ago. His 80C investment saves him zero rupees of tax. The agent knows the regime exists. The pitch has simply chosen not to.

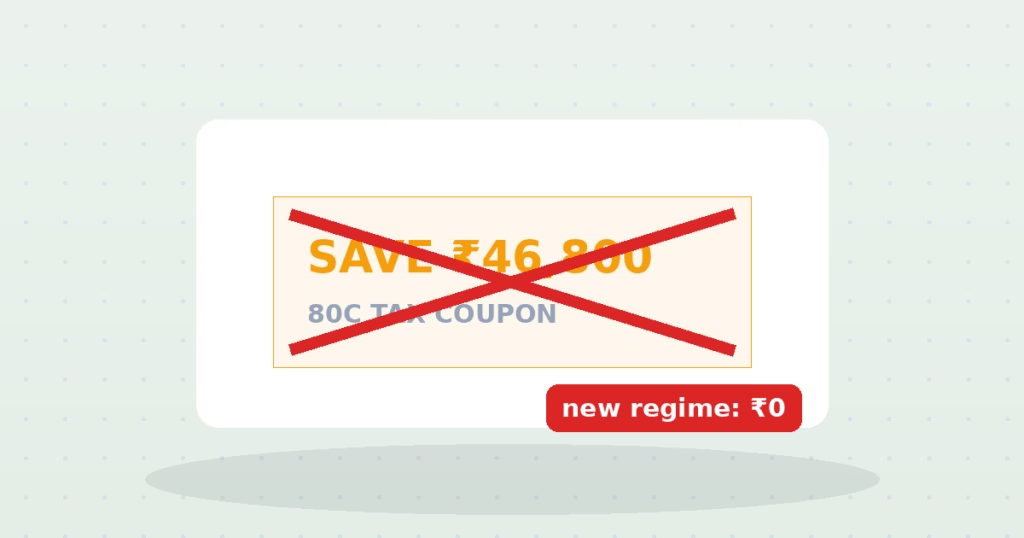

The new regime — now the default, with lower slabs and almost no deductions — quietly ended the tax case for an entire product shelf: 80C insurance policies, ELSS lock-ins, tax-saver FDs sold on the phrase “save ₹46,800”. That phrase was always the old regime’s arithmetic at the 31.2% slab. For a new-regime taxpayer it is not an exaggeration; it is fiction. Yet the January machinery still runs, because commissions did not read the Finance Act: endowments still close on “tax benefit”, tax-saver FDs still lock five years of liquidity for a deduction the buyer cannot claim, and the customer discovers the arithmetic at filing time, if ever.

That is not a rhetorical question — it is a computation. The old regime with full deductions still wins for some heavy-deduction households (big home-loan interest, HRA, stacked 80C/80D); the new regime wins for most others precisely by paying you to stop buying deduction products. Our income tax calculator runs both regimes side by side on your real numbers — the sixty seconds that should precede any January signature.

Covers salaried individuals under 60 for FY 2026-27 (AY 2027-28) — Budget 2026 kept the slabs unchanged from FY 2025-26, so the same numbers apply to both years: new-regime standard deduction ₹75,000, rebate to ₹12L taxable with marginal relief (§87A of the old Act, §157 under the Income-tax Act 2025 in force from April 2026); old-regime standard deduction ₹50,000, rebate to ₹5L; 4% cess. Capital gains (taxed at their own rates — 12.5% equity LTCG beyond ₹1.25L, 20% STCG) and surcharge edge-cases aside. Confirm with a tax professional before filing.

Here is the healthy part of the earthquake: stripped of the tax costume, each product faces its naked question. ELSS remains a decent equity fund — compare it as one, against open funds without lock-ins. Tax-saver FDs become ordinary FDs with handcuffs. And 80C endowment policies lose the only argument they ever had; at 4–6% returns, “but tax saving” was carrying the entire sale. If your investment only made sense with the deduction, it never made sense.

Before any “tax-saving” purchase: run both regimes in the calculator above and establish whether a deduction is even worth anything to you. If you are new-regime, the correct January ritual is nothing — invest on merit, any month you like, in anything without a lock-in bribe. If you are old-regime by calculation, fill 80C with the honest end of the shelf (PPF, ELSS chosen as a fund) and never with insurance wearing an investment costume. And when the agent calls, one question: “under which regime does this save me tax, and have you asked which one I use?”

Salaried taxpayers can generally choose annually at filing; business income faces restrictions on switching back. Either way, the choice is arithmetic, not identity — recompute when life changes.

As a tax product for new-regime users, yes. As a diversified equity fund with a 3-year lock-in, it must now beat funds without one — a competition it no longer automatically wins.

Disclaimer: This article is for general information only and is not financial or tax advice. Consult a qualified advisor before making investment or tax decisions.

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

Fear sells early claiming — a permanent 30% cut to dodge a hypothetical 20% one. Run the break-even…

The default fund stacks a wrapper fee on underlying fees — $118,000 over a career for a rebalancing…