The Refinance Treadmill: Lower Payment, Longer Sentence

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

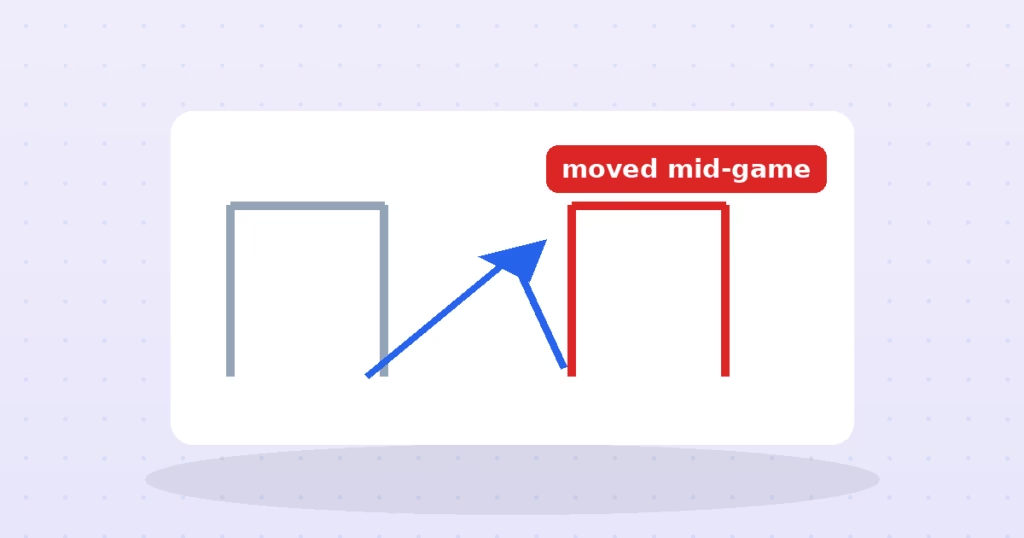

Manohar bought a flat in 2015 for ₹1 crore — not as a trader, as a man who wanted his family under its own roof and believed the tax rules he could read. Those rules said: when you sell, inflation’s share of the “gain” is not income; indexation will strip it out before tax. In July 2024, mid-game, the goalposts walked: indexation on property gains was abolished for the road ahead, replaced by a flat 12.5% on the nominal gain. Sell in 2030 for ₹2 crore and the arithmetic says Manohar made ₹1 crore. The groceries say otherwise.

At 5% inflation, ₹1 crore of 2015 money is about ₹2.08 crore of 2030 money. Manohar’s sale at ₹2 crore is, in purchasing-power truth, a small loss — he can buy slightly less house than he sold. The new regime taxes him ₹12.5 lakh anyway, on a “gain” that is entirely the rupee shrinking. Indexation existed precisely to prevent this — it was the tax code’s admission that inflation is not income. Removing it converts the government’s own currency debasement into a taxable event, payable by whoever held an asset longest.

The 2024 change initially applied the new math even to properties bought long ago — repricing decades of decisions made under written rules — until protest extracted a partial fix: owners of property bought before 23 July 2024 may compute tax the old way or the new, whichever is lower. A fair patch, and an instructive one: the fix itself concedes the original move repriced the past. The durable lesson is not about one budget; it is that tax regimes are variables, not constants, and thirty-year plans built on this year’s fine print carry an unpriced risk line.

Rules reflect the post-July-2024 capital-gains regime as applicable in FY 2026-27, with the 4% cess included in the rates shown. Not covered: the 20%-with-indexation option available to resident individuals for property bought before 23 July 2024 (compute both and pick the lower — a CA can help), unlisted shares, foreign assets, and the §54/54F/54EC reinvestment exemptions that can wipe out property LTCG if you reinvest in a home or specified bonds. Verify large transactions with a tax professional.

If you bought before the cutoff, run both computations at sale time — old (indexed, 20%) versus new (nominal, 12.5%) — and elect the cheaper; our calculator handles the comparison. Keep every cost record: purchase deed, stamp duty, improvement bills — indexation or not, cost basis is money. Use the reinvestment shelters (Section 54 family) when actually buying again. And across your whole plan, prefer flexibility to fine-print dependence: the rule that giveth was amended once and can be amended again — in either direction.

No — for assets that beat inflation hugely, the lower flat rate can win. It is worst exactly where holding was longest and appreciation was modest — the profile of an ordinary family home. That inversion is what stings.

Model returns net of the new tax and real inflation before comparing against financial assets — the calculator above does the honest version. Sentiment builds homes; arithmetic should size them.

Disclaimer: This article is for general information only and is not financial or tax advice. Consult a qualified advisor before making investment or tax decisions.

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

Fear sells early claiming — a permanent 30% cut to dodge a hypothetical 20% one. Run the break-even…

The default fund stacks a wrapper fee on underlying fees — $118,000 over a career for a rebalancing…