The Refinance Treadmill: Lower Payment, Longer Sentence

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

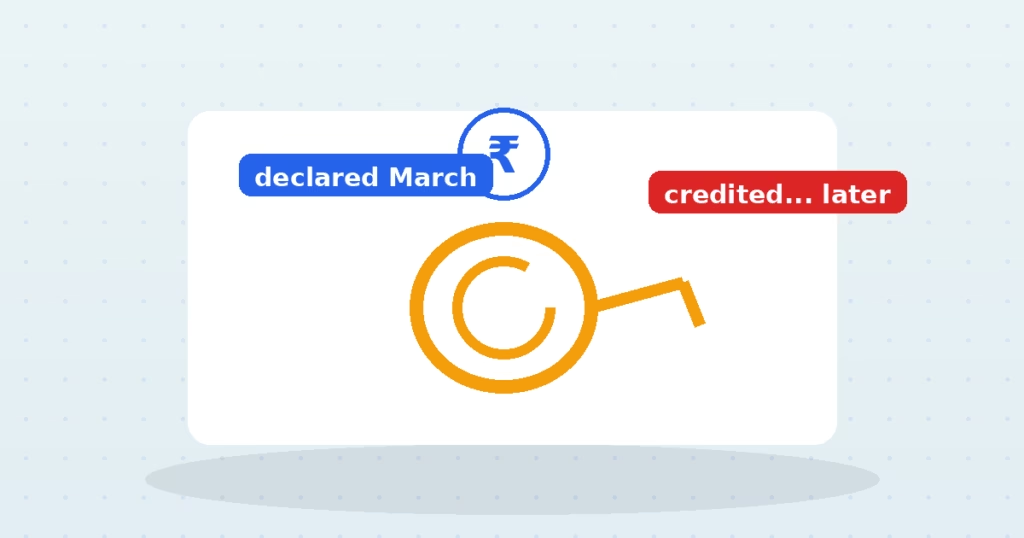

Ritu’s EPF passbook is a study in patience. The financial year ends in March; the interest rate is declared with ceremony; and the actual credit into her account arrives… whenever it arrives — routinely months later, sometimes with the next year knocking. The press release is punctual. The money is not. And in compounding, when is money: interest that lands late is interest that missed months of earning interest on itself.

EPF interest is computed on monthly running balances but credited as a lump annually — after the rate is ratified through a committee-and-ministry relay that treats the calendar as advisory. In several recent years, tens of crores of accounts saw interest credited two, three, even eight months after year-end (software upgrades and tax-rule changes have all taken turns as the reason). EPFO’s standard reassurance — “no loss, interest is calculated from the due date” — is true for the year in question and quietly false across time: until credited, the amount is not in your balance earning the next cycle’s interest, and for anyone who withdraws or transfers in the gap, the absence is very real.

Take a ₹10 lakh balance earning 8.25%: the year’s interest is ₹82,500. Credited 8 months late, that sum sat out roughly ₹4,500 of its own earning time. Small — once. Repeat the pattern across a 20-year career of growing balances and the cumulative drag compounds toward ₹2 lakh+ for a diligent saver who did everything right except control a back office.

The delay is symptomatic of a monopoly’s relationship with its members: you cannot switch providers, so punctuality is a courtesy, not a competitive necessity. The same institution charges employers penalties for late deposits — the standard it applies inward is gentler. None of this is scandal; all of it is drag, and drag is the tax nobody legislates.

Simplified: assumes 12% employee + 3.67% employer contribution on Basic + DA every month (the employer's other 8.33% funds the separate EPS pension, not this corpus), interest compounded monthly at the rate you set, and Basic + DA stepping up once a year by your increment. Real EPF also credits interest on the actual monthly running balance per year-end rules and is subject to the wage ceiling for the EPS split on higher salaries — treat this as a close estimate, not a statement.

Tax: EPF is EEE for most people — contributions get 80C (old regime), and both interest and the retirement withdrawal are tax-free after 5 years of continuous service. Two exceptions worth knowing: (1) if your own contribution exceeds ₹2.5L in a financial year, the interest earned on the amount above that limit is taxable at your slab every year (the banner above tracks this from your inputs); (2) withdrawing before 5 years of service makes the corpus taxable and attracts 10% TDS if it exceeds ₹50,000 — submit Form 15G/15H if eligible. Employer contributions above ₹7.5L/yr across EPF+NPS+superannuation are also taxable as a perquisite.

Check your passbook every quarter (the EPFO portal and UMANG app both show it) — not to fix EPFO, but to catch your side’s failures early: employer deposits missing or late are far more damaging and fully actionable. Reconcile the annual interest line when it lands; raise a grievance on the EPFiGMS portal if a cycle looks skipped. Before any withdrawal or transfer, time it after the credit hits, not before. And diversify your retirement plumbing — NPS and your own SIPs answer to market hours, not committee calendars.

No — 8%+ tax-free with sovereign character remains excellent. The lesson is narrower: institutional promises have operational lags, and your plan should carry a margin for them.

Worse — that is your money missing its earning window monthly, and it is enforceable. The passbook shows deposit dates; a pattern of lateness is a formal grievance, and EPFO does pursue employers on it.

Disclaimer: This article is for general information only and is not financial or tax advice. Consult a qualified advisor before making investment or tax decisions.

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

Fear sells early claiming — a permanent 30% cut to dodge a hypothetical 20% one. Run the break-even…

The default fund stacks a wrapper fee on underlying fees — $118,000 over a career for a rebalancing…