The Refinance Treadmill: Lower Payment, Longer Sentence

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

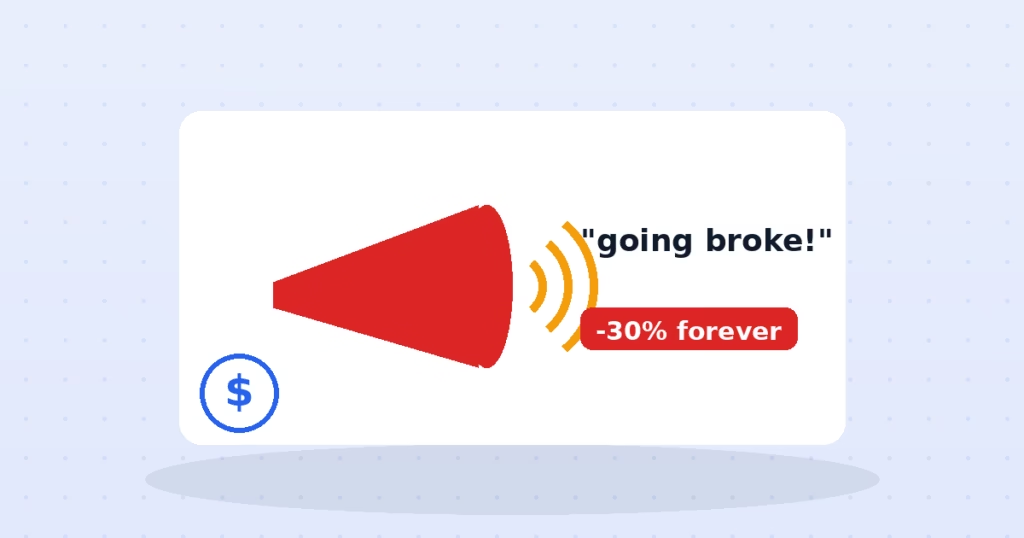

The seminar was free, the dinner was free, and the message was urgent: “Social Security is going broke — claim at 62, get yours while it lasts.” Frank, newly 61, felt the fear do its work. What the presenter did not dwell on: claiming at 62 locks in a permanent ~30% cut versus his full benefit, the “bankruptcy” he described actually projects as a roughly 20% shortfall if Congress literally never acts, and the annuity brochure waiting under his chair pays the presenter either way. Fear had a business model, and Frank was its dinner guest.

The claiming decision is the largest annuity purchase of most American lives, made once, irreversibly (after a short window). At full retirement age, Frank’s benefit is $2,000; claiming at 62 pays about $1,400 forever; waiting to 70 pays about $2,480 forever — inflation-adjusted, government-guaranteed, spouse-protecting. Delayed credits are, by wide consensus, among the best annuity deals available in America at any price. Which is exactly why products competing with them — immediate annuities, “income plans”, assets-under-management pitches — lean on the one lever that reliably beats arithmetic: dread.

Yes, claiming early means more checks. The crossover lands around age 80 — beyond which the age-70 claimer wins by widening margins for life. An average-health 62-year-old has strong odds of seeing 85, by which point early claiming has cost roughly $60,000 — and for married couples the stakes are higher still: the survivor inherits the larger of the two benefits, so one spouse’s early claim can cut the other’s income for decades.

The trust-fund projections describe a funding gap in the mid-2030s that, absent any legislation, would force benefits to roughly 77–80% of scheduled levels — a serious policy problem, and nothing resembling zero. Claiming early to “beat” a hypothetical 20% cut by accepting a certain 30% cut is the pitch’s central magic trick; said plainly, it collapses.

Uses simplified, illustrative bend points based on the Social Security Administrations own published benefit formula, which is adjusted for wage inflation most years -- your real benefit depends on your actual 35 highest-earning years, indexed for inflation, which this single average-earnings input cannot fully capture. For your real estimate, check your account at ssa.gov, which uses your actual earnings record.

Run your real numbers in the calculator above — your benefit at each age, your health honestly assessed, your spouse’s situation included. Bridge strategies beat panic: many households spend modest savings from 62–70 to “buy” the maximum benefit, the cheapest inflation-proof annuity in existence. And at any free dinner, apply the one rule: whoever profits from your claiming date is not your actuary. Delay is not always right — poor health and cash need are real reasons — but fear never is.

Every serious reform proposal grandfathers people at or near retirement — cutting checks of current claimants is political kryptonite. Reforms historically land on younger cohorts, gradually.

Within 12 months you can withdraw the application (repaying benefits) and reset; after that, suspending at full retirement age can still earn delayed credits on the suspended months. Options narrow, but exist.

Disclaimer: This article is for general information only and is not financial or tax advice. Consult a qualified advisor before making investment or tax decisions.

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

The default fund stacks a wrapper fee on underlying fees — $118,000 over a career for a rebalancing…

Interest plus 1%: enough to keep you current, never enough to free you. $5,000 becomes 19 years and…