The Refinance Treadmill: Lower Payment, Longer Sentence

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

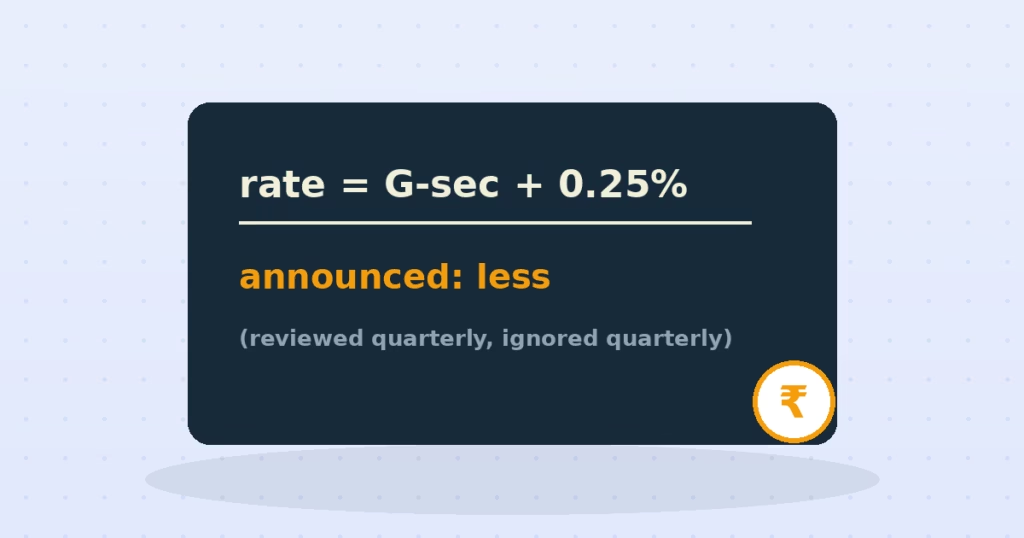

Every quarter, a committee meets to set the PPF rate, armed with a formula the government itself adopted: small-savings rates should track government bond yields, with a small bonus — for PPF, the 10-year G-sec yield plus 25 basis points. Every quarter, crores of savers’ returns hang on the meeting. And for years at a stretch, the announced rate has sat below what the formula prescribes — rounded down, frozen, “held steady” — while the same government’s borrowing costs set the benchmark. The formula exists. The following of it is optional. Guess in which direction the option is exercised.

The Shyamala Gopinath committee framework (2011) was meant to end politics in small-savings rates: benchmark to G-sec yields, adjust quarterly, publish the logic. In practice, rates are “reviewed” quarterly and frequently left unchanged even when the formula points up — because every 0.25% on the small-savings pool costs the exchequer real money, and savers do not march. When yields fall, cuts have historically arrived with more punctuality. The asymmetry will feel familiar to anyone who has watched banks pass on rate hikes versus rate cuts: the same physics, operated by the referee.

Small numbers, long horizons: ₹1.5 lakh a year into PPF for 15 years at 7.1% builds about ₹40.7 lakh; at the 7.35% a formula-faithful regime might pay, about ₹41.6 lakh. The ₹89,000 difference is one family’s withheld bonus — multiply by the tens of millions of PPF, SSY, SCSS and NSC accounts and the “rounding” becomes one of the quieter fiscal instruments in the country: a tax on patience, collected from its most disciplined citizens.

None of this makes PPF bad — EEE tax treatment (exempt on contribution, growth and withdrawal) is nearly unique, the sovereign guarantee is real, and even a shaved 7.1% tax-free beats a 7% FD taxed at slab by a wide margin. The point is subtler and more useful: treat the rate as a policy output, not a law of nature. It can drift down through your accumulation years, and your plan should not assume otherwise.

Assumes the full annual amount is deposited at the start of each financial year (the best case for interest) and compounded annually at a constant rate for the whole tenure. PPF's actual rate is set by the government every quarter and can change year to year — update the rate slider whenever it does.

Tax: PPF is one of the very few EEE instruments left: the deposit qualifies for 80C (old regime, up to ₹1.5L/yr), the interest accrues completely tax-free, and the entire maturity is tax-free too — no TDS, and it doesn't even need to be offered to tax. Under the new regime you lose the 80C deduction on the way in, but the interest and maturity stay tax-free either way. That makes PPF's effective pre-tax-equivalent yield for a 30%-slab investor roughly 1.45× the headline rate when comparing against an FD.

Max the PPF in April, not March — a full year’s interest on the full amount, every year, compounds into lakhs across the account’s life. Track the quarterly announcements (two minutes, four times a year) so rate drift enters your planning early. Ladder across small-savings products — SSY for daughters and SCSS at 60 carry their own, usually better, spreads over the formula. And hold the system to its own paper: the formula is public; quoting it in consultation windows and to representatives is how frozen quarters eventually thaw.

Structurally, small-savings rates follow G-sec yields downward as an economy matures. Plan conservatively: model your PPF at a rate slightly below today’s and be pleasantly surprised.

Both, for different jobs: PPF is the guaranteed, tax-free floor of a portfolio; equity is its growth engine. The mistake is asking either to do the other’s work.

Disclaimer: This article is for general information only and is not financial or tax advice. Consult a qualified advisor before making investment or tax decisions.

Each refi resets the interest-heavy years and rolls in fresh costs. Keep the rate; keep the clock honest.

Fear sells early claiming — a permanent 30% cut to dodge a hypothetical 20% one. Run the break-even…

The default fund stacks a wrapper fee on underlying fees — $118,000 over a career for a rebalancing…